- Zivoe Newsletter

- Posts

- Zivoe Crosses $1.36M in Revenue | Tokenized Private Credit and the MCA Opportunity

Zivoe Crosses $1.36M in Revenue | Tokenized Private Credit and the MCA Opportunity

Your Portal to Tokenized Private Credit

Thor Abbasi

March 31, 2026

Where We Stand

Zivoe has now generated $1.36M in cumulative protocol revenue since launching at the end of 2024, with $6.93M in TVL. Every scheduled distribution since our first in November 2024 has arrived on time, across 16 consecutive months of operation.

The State of Tokenization

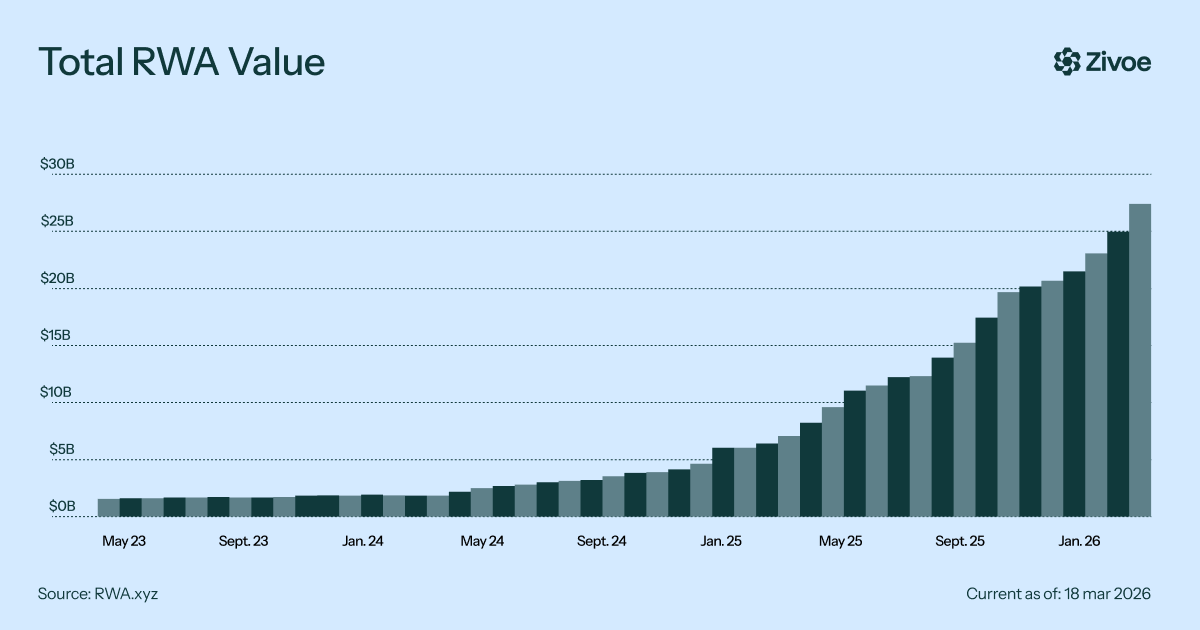

On-chain tokenized real-world assets have crossed $27 billion, up from approximately $6.6 billion a year ago, nearly a fourfold increase. The question is no longer whether tokenization will reshape capital markets, but how fast. A few recent examples:

BlackRock CEO Larry Fink called tokenization the future of financial markets, comparing it to the internet in 1996.[1]

NYSE partnered with Securitize to build the infrastructure for blockchain-native securities trading.[2]

BNY Mellon's CEO named major banks as the primary vehicle for integrating crypto and traditional finance.[3]

The Reserve Bank of Australia estimated $16.7B in annual economic gains from tokenization and moved to active implementation.[4]

SEC Chair Paul Atkins announced a forthcoming innovation exemption to reduce regulatory barriers for tokenized assets.[5]

Private credit remains the largest category of tokenized real-world assets. Capital moving on-chain is looking for returns backed by real economic activity. Within private credit, not all strategies are equally positioned for this moment. That is where the case for short-duration lending begins.

The Case for Short-Duration Private Credit

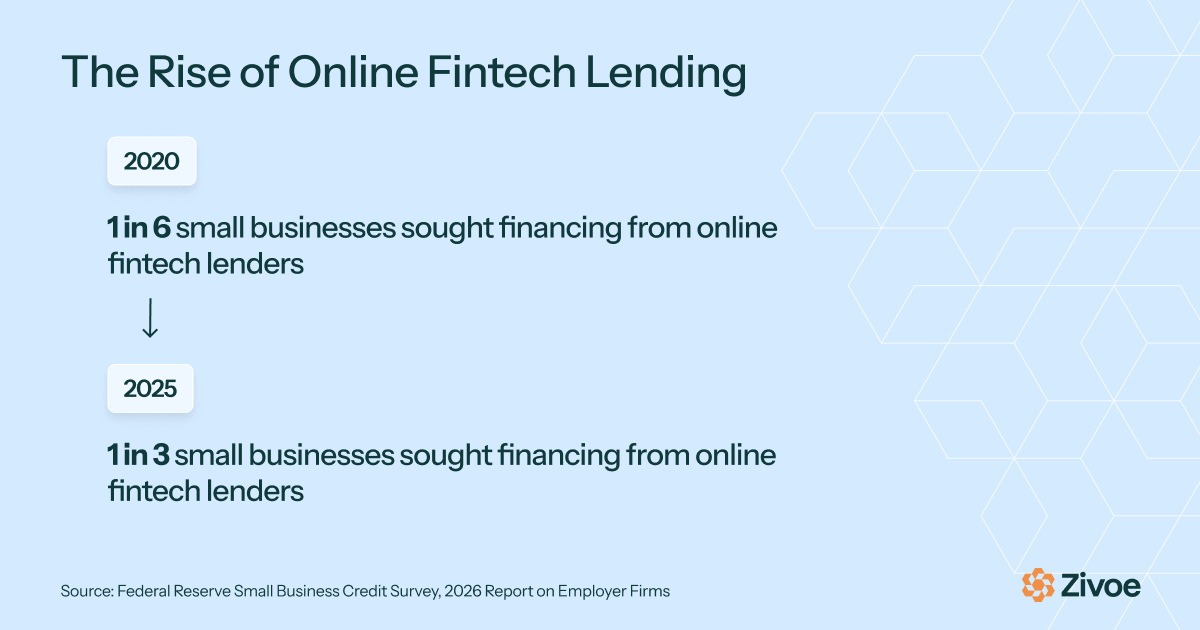

According to the Federal Reserve's most recent Small Business Credit Survey, 86% of small businesses use financing on a regular basis.[6] It is not a one-time need. It is an ongoing part of how these businesses operate. Against that backdrop, small businesses are turning to alternative lenders at a growing rate. The share seeking financing from online fintech lenders rose from 17% to 29% over the last five years, a shift that reflects structural bank retrenchment, not a temporary trend. Merchant cash advance is already the fourth most commonly used financing product among small businesses, with 7% using it on a regular basis, and that share is growing.

Merchant cash advance is the purchase of a portion of a business's future receivables at a discount, repaid through regular deductions tied directly to that business's cash flow. Durations generally run three to six months. Repayment is tied to revenue performance rather than a fixed calendar schedule. When small business credit tightens, MCA providers tend to see more volume and greater selectivity.

Short-duration assets like MCA can be particularly well suited to on-chain capital markets. When underlying receivables recycle every three to six months, LPs can benefit from faster capital availability and more frequent performance visibility than longer-dated private credit strategies typically allow. Short-duration strategies can generate frequent, observable cash flow events that are well suited to on-chain reporting and settlement, with capital recycling more regularly than in longer-dated credit structures. As on-chain infrastructure matures, there is potential for greater transparency and efficiency across each stage of the lending cycle.

Zivoe is connecting on-chain capital to this opportunity through partnerships with an established MCA originator with a multi-year track record and billions in cumulative origination volume.

What's Next

Our focus is on growing TVL, deepening our MCA strategy, and building toward greater protocol transparency as we scale.

If you are interested in learning more about participating as a liquidity provider or exploring a partnership with Zivoe, reach out at [email protected] or message @thorabbasi on Telegram.

Reply